Going global: Can the People’s Republic of China help FDI recover from the crisis?

The 2008 global financial crisis (GFC) and the sovereign debt crisis in the European Union (EU) weakened the risk appetite of United States (US) and European investors. Is the world now looking toward emerging economies such as the People’s Republic of China (PRC) to make up for depressed investment flows from the North in the post-crisis era? The forms that these flows have taken suggest that this is indeed occurring.

FDI on the rise

The share of developing and transition economies in global foreign direct investment (FDI) outflows rose from 16% in 2007 to 27% in 2011, reaching the second highest level recorded. In 2011, PRC’s multinational corporations (MNCs), who were the major drivers for the strong growth in FDI outflows, continued their buying spree, actively acquiring overseas assets in a wide range of industries and countries, overtaking Japanese companies to become the sixth largest world investor.

The ‘Going Global’ pace of PRC’s MNCs has resulted in a dramatic increase in outward FDI in the past decade. Outward FDI has increased from less than $10 billon in the early 2000s to $74.7 billion in 2011 with 51% average growth rate since 2003 (Figure 1). This phenomenal increase has turned the PRC’s international capital flow from one-way inward FDI into a two-way outward and inward FDI (Figure 2).

Figure 1: Outward Foreign Direct Investment of the PRC, 1982-2011 ($ billions)

Source: Data from 1982-2001 are from the PRC’s Balance of International Payments of State Administration of Foreign Exchange (SAFE) database; Data from 2002-2011 are from various issues of the Ministry of Commerce’s (MOFCOM) Statistical Bulletin of the PRC’s Outward Foreign Direct Investment.

Note: Data from 1982-2005 are the PRC’s Outward FDI of non-financial sectors; Data from 2006-2011 are the PRC’s Outward FDI of the whole industry. The data is still comparable between the two periods as Outward FDI of the financial sector before 2006 was insignificant.

Figure 2: Inward and Outward Foreign Direct Investment of the PRC, 2000-2011 ($ billions)

Sources: Outward FDI data are from State Administration of Foreign Exchange (SAFE) and Ministry of Commerce (MOFCOM), Inward FDI data, are from the PRC Statistical Yearbook.

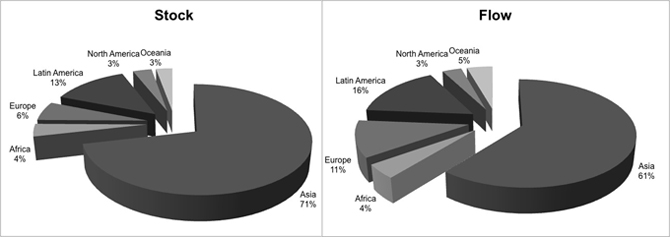

The direction of the PRCs FDI flows indicates the ability of Chinese firms to manage high risk in less developed countries (LDCs). UNTCAD estimates that by the end of 2011, more than 13,500 of the PRC’s domestic investing entities had established about 18,000 overseas enterprises, spreading across 177 countries with 72% coverage globally. Most of the PRC’s FDI was distributed in Asian and Latin American developing countries. Although developing African countries only accounted for 4.3% of the PRC’s total FDI in 2011, they absorbed nearly 7.4% of total world FDI in 2011, which ranked fourth in flow, and sixth in stock.

Figure 3: Regional Distribution of the PRC’s FDI by Flow and Stock, 2011 (Percent)

Source: Statistical Bulletin of the PRC’s Foreign Direct Investment(2012) by MOFCOM.

Location Strategies for PRC MNC’s are changing

Recent trends and features of the PRC’s FDI have shown that central level and state-owned enterprises (SOEs) still dominate, but with a decreasing trend in terms of total volume. These SOEs engage in large-scale merge and acquisition activities, seeking strategic assets and resources in developed countries (such as US and Europe) and resource-rich countries (such as Africa). As the ultimate owner of SOEs, the PRC has effectively involved and supported (both directly and indirectly) the process of international investment decisions so that ‘firm-specific advantage’ becomes a ‘country-specific advantage.’ The geographic and psychic distance features of these MNCs are at odds with aspects of the standard model of FDI from other developing countries whose FDI mostly locate in other neighboring developing countries with similar culture and customs.

Meanwhile, the same ‘Going Global’ strategy has formed a more liberalized framework for FDI which acts as an indirect ‘hands-off’ supporter encouraging private-owned enterprises (POEs) to invest abroad since 2003. Therefore, provincial level non-state-owned enterprises (NSOEs) actually predominate FDI, and with an increasing trend in terms of the number of domestic investment entities. These are primarily small-scale investors, setting up new plants to take advantage of low labor costs in neighboring Asian countries. The rising importance of NSOEs indicates that geographic and psychic proximity is increasingly important to the motives of new PRC MNCs, which is more consistent with classical international investment theory.

Conclusion

The PRC is now emerging as the next new power of world investors. Formed by SOEs eager for strategic assets and resources, together with POEs coping with rising labor costs, the ‘Going Global’ strategy not only serves as an important way for PRC to restructure the economy and sustain long-run economic growth, but also supports global investment and economic growth recovery in this post-crisis era.