India’s Iconic IT Industry: A 21st Century Tale Beyond the Numbers

The Information Technology (IT) and IT-enabled Services (ITeS) industry in India is the envy of many a nation. Often labelled the world’s back-office, India is the outsourcing destination of choice today for a wide portfolio of services. The aggregate turnover of the industry (excluding hardware) in the fiscal year ending March 2014 was US$105 billion, an overwhelming $86 billion being earnings from overseas that were critical to defray India’s burgeoning current account deficit.

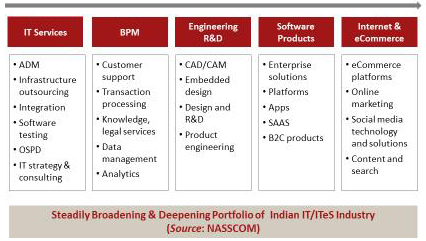

Figure 1. Portfolio of Indian IT/ITeS Industry

Source: NASSCOM

The workforce directly employed by the sector crossed 3 million with the vast majority in their 20’s and a third being women. Moreover, the employment multiplier is estimated to be in the range of 3 to 4 making the industry the primary engine fuelling urban job opportunities in the country, admittedly concentrated to date in six metropolitan centres where the physical transformation of the urban landscape has also been palpable. In turn these prospects have stimulated the demand for secondary education and hearteningly so for girls. Concurrently, the private sector has driven the smart expansion in supply of tertiary education as well.

Impressive as they may be, the numbers above belie the salience of the IT/ITeS industry to India’s economic performance. It is the vanguard of the services export revolution whereby “modern services” comprising software, financial, communication and business services now comprise over three-quarters of India’s services exports. In terms of domestic value-added, the level around 60% is a multiple of the average for merchandise exports.

The industry also proved to be surprisingly resilient during the recent global economic crisis despite the heavy concentration of its markets in North America (60+%) and Western Europe (30%) and the large share of the banking and financial services industry. The resilience, easily explained with the benefit of hindsight and careful reflection on the economics of both demand and supply, is reassuring in light of the perceived vulnerability to volatility in the global economy. Similarly on the domestic front, the IT/ITeS sector has demonstrated a sustained ability to hurdle structural deficiencies in the Indian economy such as those related to infrastructure and education as well as to weather “policy paralysis” that stymied business in recent years.

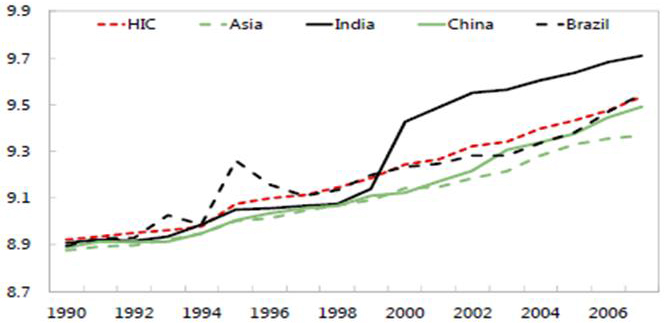

Arguably the most significant contribution to the nation’s long-term development is its role in the dramatic increase in “sophistication” of India’s service exports. Recent economic research has authoritatively established that it is not just how much a country exports but more importantly what it produces that matters for sustaining economic growth. Two factors that have been key are the abundant availability of talent (buttressed considerably by the industry’s acquired competence in skilling and re-skilling staff) and the attraction of Foreign Direct Investment (FDI) including captive subsidiaries termed Global In-house Centres (GIC) where India's IT/ITes sector continues to dominate including in new industry verticals as well as functions (e.g. engineering design, R&D).

Figure 2. Sophistication of Services Exports

S

S

ource: IMF staff estimates

The increasingly wide range of business lines and higher complexity of activities in various segments of the Indian IT/ITeS industry demonstrate the deepening technological capabilities that spill over into adjacent sectors and increase their competitiveness. Indeed, going forward, leveraging the IT sector, both in terms of direct enhancement of productivity as well as its brand value in global markets will be critical to achieving breakthrough in the export performance of most other services such as business, professional, audio-visual, health, education as well as tourism, travel and logistics where recent trends have otherwise not been too encouraging.

The IT/ITeS sector has also spawned an extraordinary burst of entrepreneurial activity seeking to emulate Silicon Valley success stories. Combined with the technological capabilities alluded to above, innovation has received a tremendous fillip and is beginning to capture the imagination of established business leaders and government policy makers alike. Most gratifying is the remarkable number of efforts that focus on inclusive development by addressing the needs of people with limited ability to pay especially related to health, education, transport and communications. Interestingly, this has reportedly also spurred movement among multinational firms to locate their product development hubs for low-income markets in India.

The 21st century tale so far clearly indicates promising prospects for the Indian IT/ITeS industry going forward. It should, however, not be a cause for complacency. Although, India is perhaps the only country (besides the US, of course) that has an established presence in all parts of the global offshore services value chain, competition is emerging in each segment form different quarters. Secondly, the advent of disruptive technologies (e.g. Social media, Mobile devices and applications, Analytics and Cloud Computing – SMAC for short) are causing market upheaval and business uncertainty. There are opportunities as well, such as advantages offered by Tier 2 locations but these require supportive policy frameworks and conducive business environments. Topics for another day….

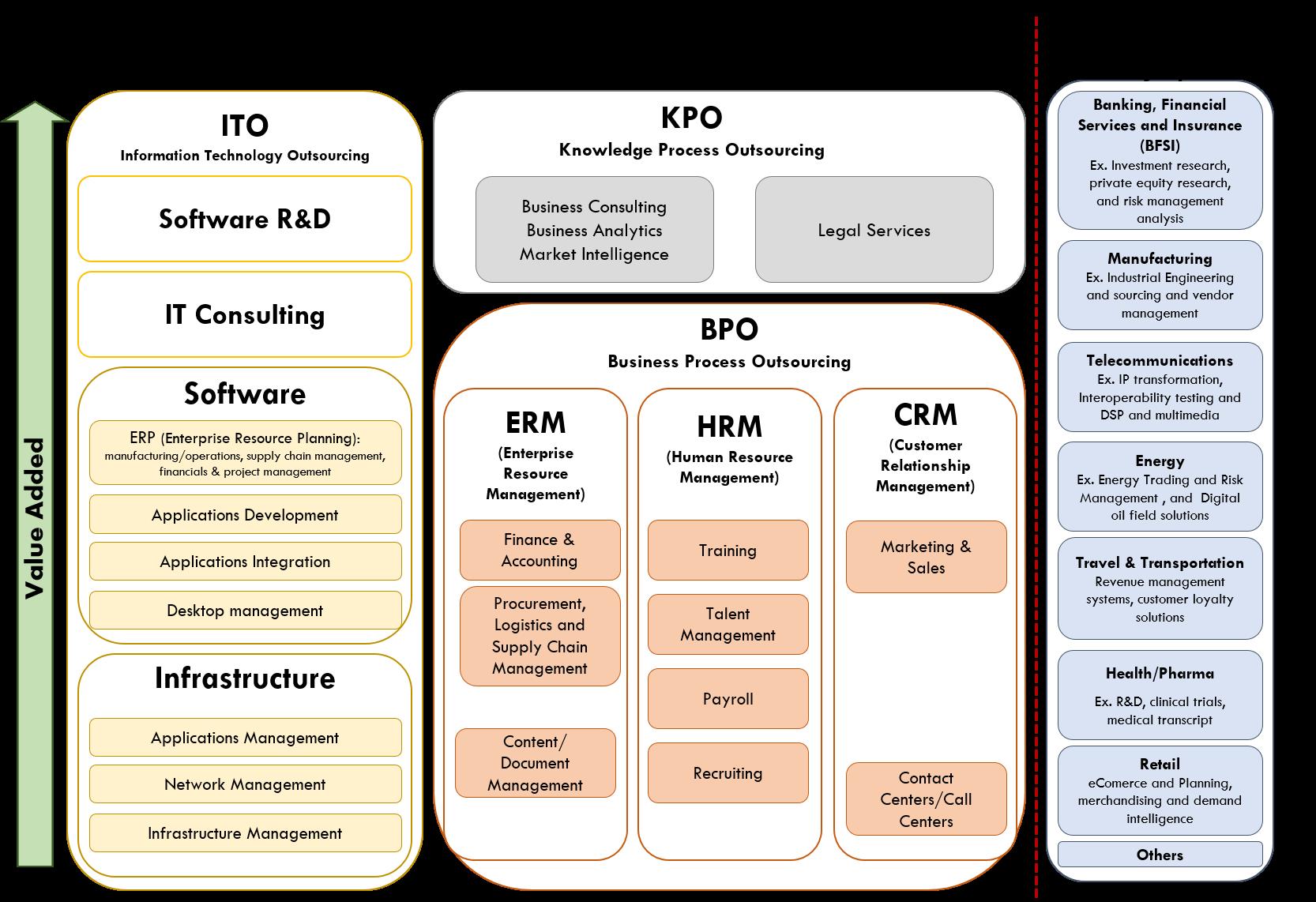

Figure 3. Global Offshore Services Value Chain

Source: CGGC (2010)

*Dr. Anupam Khanna was Chief Economist & Director-General, Policy Outreach at NASSCOM, the association of the IT/ITeS industry in India.